Two Signals Push Mortgage Rates Higher

Mortgage rates moved higher this week, and that matters whether you are buying, selling, or trying to time your next move.

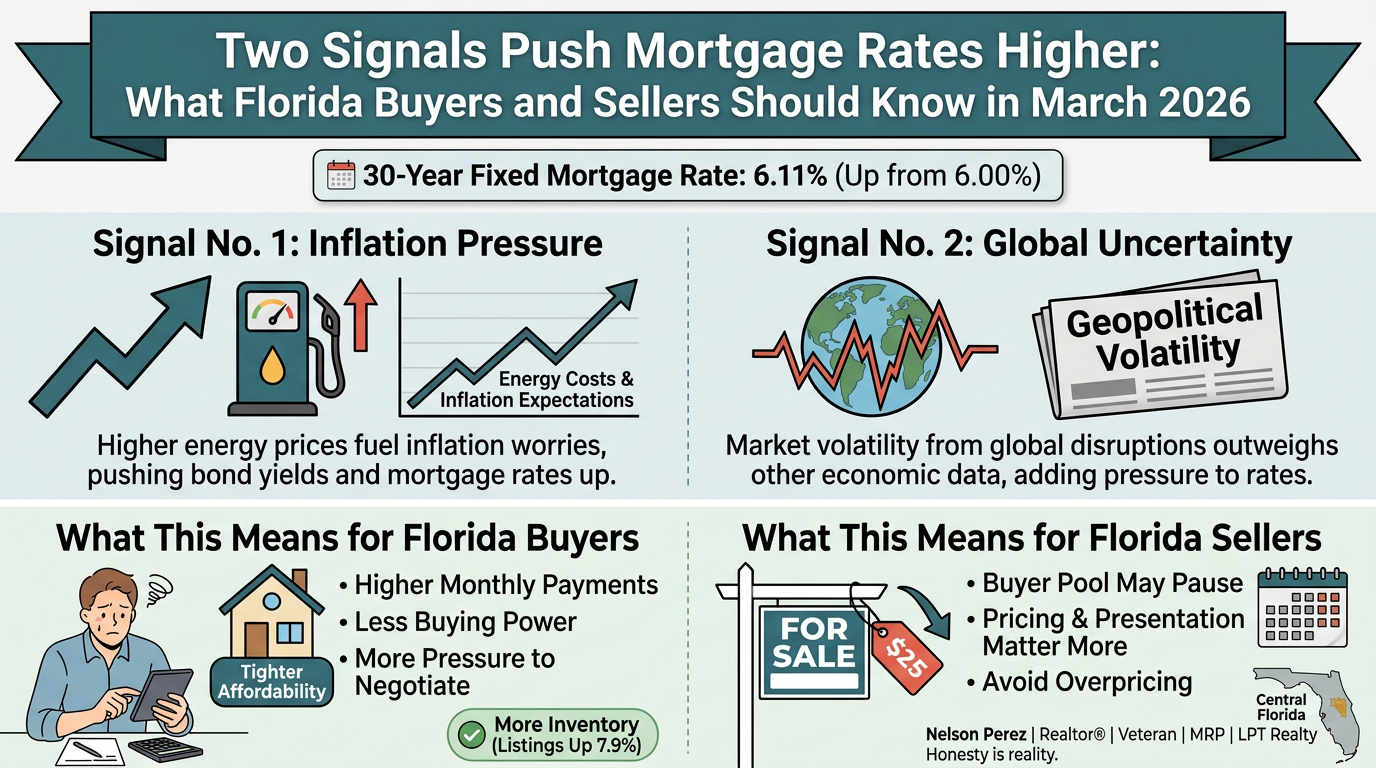

Freddie Mac reported the average 30-year fixed-rate mortgage at 6.11% as of March 12, 2026, up from 6.00% the week before. The 15-year fixed average also moved up, to 5.50% from 5.43%. Freddie Mac said rates “inched higher” as housing activity picked up.

So what pushed rates up?

Right now, two signals are doing most of the work:

Higher inflation pressure and market volatility are tied to global uncertainty. Realtor.com said this week’s jump reflected volatility from geopolitical uncertainty outweighing softer labor-market data, while Mortgage News Daily pointed to higher energy prices and inflation expectations as key pressure points.

At Honesty Is Realty, I like to keep this simple. Honesty is reality. Rates do not move because of one headline. But when inflation worries and market uncertainty show up together, mortgage rates usually feel it.

Signal No. 1: Inflation Pressure Is Pushing Borrowing Costs Up

Mortgage rates tend to move with the bond market, and bonds usually do not like inflation.

Mortgage News Daily said higher energy costs have been fueling inflation expectations, and that tends to push rates higher. Earlier in the month, it also said oil-price spikes were spilling over into the bond market because higher oil can feed inflation concerns.

That is a big deal for housing because even a small rate increase changes affordability. A move from 6.00% to 6.11% may not sound huge, but when buyers are already budget-sensitive, every fraction of a point matters. Freddie Mac’s weekly survey confirms that the move higher already happened this week.

Signal No. 2: Global Uncertainty Is Adding Volatility

The second signal is broader market uncertainty.

Realtor.com said mortgage rates jumped this week because volatility caused by geopolitical uncertainty outweighed relatively soft labor-market data. Mortgage News Daily also described the rate environment as driven by “volatile crosscurrents,” with global disruptions and energy-related inflation concerns pushing in the wrong direction for borrowers.

That is why rates can rise even when one economic report looks helpful on the surface. Markets are forward-looking. If investors think inflation risks or global instability could stick around, mortgage pricing can move higher fast.

What This Means for Florida Buyers

For buyers in Florida, especially in Central Florida, Polk County, Osceola County, Davenport, Kissimmee, ChampionsGate, Lakeland, and Winter Haven, higher rates mean one thing first:

Affordability gets tighter.

A slightly higher rate can mean:

-

A higher monthly payment

-

Less buying power

-

Tougher debt-to-income ratios

-

More pressure to negotiate price or seller concessions

The good news is that this is not the same market buyers faced when inventory was tighter. Realtor.com reported active listings were up 7.9% year over year in February 2026, giving buyers more choices than they had a year ago.

So yes, rates are up. But buyers may still have leverage in other parts of the deal.

What This Means for Florida Sellers

For sellers, this rate move matters because it affects your buyer pool.

When rates rise, some buyers pause. Others lower their price range. Others become more aggressive in negotiations because monthly payment matters more than ever.

That does not mean homes stop selling. It means pricing and presentation matter even more.

In a market where buyers are comparing more homes and watching payments closely, overpricing gets punished faster. Sellers who understand that usually do better than sellers who are still chasing yesterday’s market.

Should Buyers Wait?

That depends on your full situation, not just the headline.

NAR said last week that holding near 6% had been improving affordability for millions, but this week’s move to 6.11% shows rates are still volatile and not moving in a straight line. NAR Chief Economist Lawrence Yun has also said he expects rates to trend lower over time, but not smoothly.

My take is simple:

If the payment works, the home fits, and the strategy is solid, waiting for a perfect rate can backfire.

My Straight Take

Here is the real-world version.

Mortgage rates moved higher because markets are worried about inflation and reacting to uncertainty. That is the headline. But your move should still be based on your numbers, your timeline, and your options.

For buyers, that means getting serious about:

-

Payment comfort

-

Negotiation strategy

-

Lender options

-

Seller credits

-

Builder incentives where available

For sellers, that means:

-

Pricing correctly

-

Understanding today’s buyer mindset

-

Avoiding overconfidence

-

Being prepared for payment-sensitive negotiations

Final Takeaway

The two biggest signals pushing mortgage rates higher right now are inflation pressure and market volatility tied to global uncertainty. This week, that pushed the average 30-year fixed mortgage rate to 6.11%, according to Freddie Mac.

For Florida buyers and sellers, the message is not panic.

It is this:

Be more strategic.

Rates are still moving. Inventory has improved. Buyers have more choice. Sellers need sharper pricing. And both sides need better advice than “just wait and see.”

That is where smart planning wins.

FAQs

Why did mortgage rates go up in March 2026?

Mortgage rates moved higher because of inflation concerns and market volatility tied to geopolitical uncertainty. Freddie Mac said the average 30-year fixed rate rose to 6.11% on March 12, 2026.

What are the two signals pushing mortgage rates higher?

The two main signals are inflation pressure, especially from higher energy costs, and broader market volatility tied to global uncertainty.

Are higher mortgage rates bad for Florida buyers?

Higher rates can reduce affordability and buying power, but buyers may still benefit from improved inventory and more negotiating room than they had in tighter markets.

What should Florida sellers do when rates rise?

Sellers should focus on realistic pricing, strong presentation, and understanding that buyers are more payment-sensitive when mortgage rates move up.

About Me:

Nelson Perez | Veteran & MRP Realtor® in Central Florida (Polk + Osceola)

I’m Nelson Perez, a U.S. Veteran and MRP-certified Realtor® with LPT Realty, based in Davenport, Florida. With 30+ years of construction experience and a straight-shooting negotiation style, I help buyers, sellers, and investors win across Central Florida—especially Polk County and Osceola County. “Honesty is reality.” That is how I operate: clear advice, clean communication, and strategies that protect your money.

*Trying to buy, sell, or relocate in Central Florida while rates keep moving around? Let’s talk strategy, payment options, and the best way to move without guessing.

Categories

- All Blogs (92)

- 911 (2)

- April Awareness Days (1)

- buyer (31)

- Central Florida Home Buyers (2)

- Davenport (2)

- florida market (11)

- FSBO (2)

- Home Buying Guides (7)

- Home Maintenance, (6)

- Homeownership (1)

- Knowlege is Power When it comes to todays market (2)

- Military Families (6)

- Personal Finance," "Credit Score," "Money Tips (1)

- Real Estate Market News (8)

- renting (2)

- seller (9)

Recent Posts

MRP Realtor® | Veteran Real Estate Advisor | License ID: SL3558188

+1(954) 418-2463 | nperez@axenrealty.com